Over a Barrel? The Middle East Crisis' Next Phase

Another Reshuffling of Global Energy Supply Chains

The news of the Iran crisis’s impact on oil and gas markets is challenging to follow. What is clear, though, is that more shortages or shortfalls are upon us, with Asia and Europe the hardest hit. The prices of Brent and WTI futures have finally caught up from a few weeks back at ~$114 and $105, respectively, on Monday, May 4th, midday. While the U.S. has seen the least-worst impacts, a reshuffling of global energy supply chains and energy source mixes is likely over the medium term.

Taking Stock

According to a good stocktake in The Economist on April 30th, the most likely amount of oil market shortfall has been 12.3 m/b/d, or 10% of global supply through March and April. I wrote about alternative pipelines used by Saudi Arabia and the UAE that bypass the Strait of Hormuz in an earlier article.

The value of spare capacity, mostly from them, is limited now, and a good amount of it blocked. (Ironically, a Middle East oil market expert opined about the value of spare capacity in early April, before the UAE announced the departure of OPEC for May 1.) U.S. shale is forecast to only ramp up 300,000-700,000 extra barrels per day over the next 3 to 6 months. Specifically, one Permian producer is planning an extra 50,000 of incremental production. Russia could add 300,000.

Around the world, solutions in the near term are rationing of supply and price hikes to reduce demand. Crude oil demand has been reduced in the Middle East, owing to war disruptions; roughly 50% in Asia; and the remaining from East Africa, which is dependent on the Gulf; and some Eastern Europe.

Interestingly, as noted earlier too, U.S. crude exports and refined products would be called upon.

Reuters reported on April 30th: “Total U.S. crude exports climbed to a record 6.44 million barrels per day, marking a 1.64 million bpd rise from the week prior.” See where our transport fuel exports go—mostly to Latin America and the UK, plus the Netherlands.

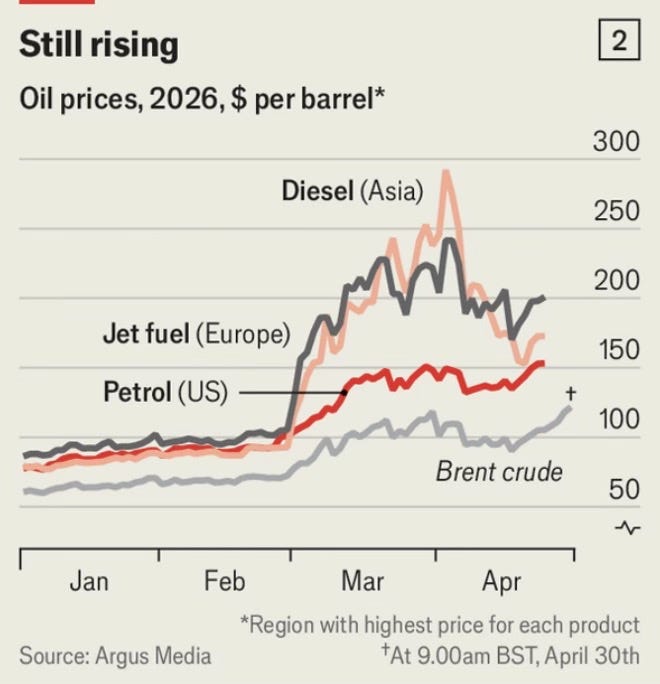

Pain points are most visible in diesel cargoes. One trader saw a $600 diesel cargo from $300 the week prior. The U.S. doubled diesel exports to Europe from January 2025 of 167,000 b/d to 396,000 in January 2026 for heating and power. Russian sanctions were the main cause of Europe’s switch to U.S. cargoes. In March, they reached 414,000.

The stocks of refined products such as petrol, diesel, and kerosene (jet fuel) are dispersed among millions of suppliers and consumers and so are not easy to measure. Demand, meanwhile, is typically inferred from data on production, trade, and storage rather than measured directly, notes The Economist in trying to sort stocks from flows.

The bankruptcy of Spirit Airlines is a definitive casualty. Air fares are rising quickly in the U.S. ahead of the summer travel season. Travelers will either choose to purchase but now for fear of higher prices, or wait and see. One might envision more road trip vacations to shorter distances.

Stocks and Flows

While the stocks reducing story is troubling, the flows story is just starting. Noted by the Economist:

“If demand destruction has reached 4m b/d over the past two months—a generous estimate—that means the world has been draining stocks by as much as 8m b/d. …If Hormuz remains closed, [sea borne trade] and releases from strategic reserves dwindle, commercial inventories will have to provide 6m-8m b/d—a pace no one considers sustainable.

One trader expected shortages to materialize within 4-8 weeks in most regions.

Crisis Strategy

There’s nothing like a crisis to create new strategies. The UAE made a timely decision to leave OPEC. Aside from Saudi Arabia, the UAE is a source of spare capacity. They will now ramp from their 3.2-3.5 m/b/d prior quota to 5 million by 2027. They could conceivably go higher. Right now, that’s market signal that others can step into rebalancing the market. Oil market producers have every incentive to not allow the demand destruction happening now to continue into the future.

The chart below reflects the impact on overall prices rose sharply with Europe’s Russian energy and gas shock. Countries are more energy efficient and have altered their supply chains too. On the flow side, I expect more shifts in energy supply chains and diversification of sources.

U.S. exports will be increasing as noted above, but their stickiness is to be determined. After Russia’s invasion of Ukraine, the U.S. increased its LNG trade considerably. There is definitely incremental activity being picked up in the U.S Gulf.

‘The crisis has pushed U.S. LNG exports roughly 1.9 Bcf/d above pre-crisis forecasts for 2026 overall, hitting U.S. infrastructure’s ceiling,’ NPR reported. In the next 1–2 years as new capacity comes online — U.S. LNG supply is forecast to grow by about 84% over the next five years, according to S&P Global Energy. However, the terminals and pipelines are inadequate to fill the 10+ Bcf/d void left by Qatar in the near term.

LNG exporters Cheneire, Woodside Energy and Venture Global have seen their stock prices rise with the large spread between U.S. gas versus European and Asian prices. While energy stocks have had a run upward, semiconductors reflective of the tech and AI trade indicate a type of momentum owing to near term trends and sentiment. Scarcity is also part of the semiconductor trade, but chips competition is changing slowly. Energy investing has nuance and changing fundamentals but commodities are its baseline.

What Matters Now?

Bottomline: In the energy space, the increased relevance of the opportunities are now more salient such as midstream and infrastructure plays connected to longer-term export opportunities. More upstream deals and consolidation will continue in U.S. oil and gas.

Markets will definitely be rebalanced based on prices ahead. Developing countries hit by the shortages the hardest will shift policies ahead incrementally. Stable, market-based economies will benefit in terms of being rewarded with new business opportunities and capital flows. The UAE’s move to align toward a more market-oriented outcome is also a sign of the times. The country has recently articulated its new plans which includes $55 billion in upstream and infrastructure development.

What comes next based on fundamentals is higher prices in places and reduced consumption that filters through everything. Can developed countries take the hit? It depends on one’s energy orientation and sound policies based on the way in which energy works, not as it is idealized. Infrastructure changes are longer lead affairs with large amounts of capital required.

Does Iran have oil markets over a barrel? Temporarily, in terms of the shock and awe, but that has largely passed for now. On a practical level, adaptation, pioneering new opportunity, and rethinking supply chains is next.