The Price of Oil is the One Ring to Rule Them All, Still

The price of oil is global and ultimately set by the long memory of market forces

There is still virtually no other price that speaks volumes about the state of global economies and geopolitics than that of oil. We are once again reminded that the price of oil is global and set by the global market. Just because the U.S. produces roughly 22-25% of oil and gas supplies globally now, thanks to a free market approach, we are unequivocally globally-connected on this one.

Crisis in oil and gas, especially of this magnitude in the Middle East, scathes all markets and countries, to greater and lesser degrees, based on their fundamentals of supply and demand and their export-import dynamics. No one is escaping inflation really.

(As of April 12th, the U.S. is forming a blockade in the Strait of Hormuz to deter Iran holding the transit way hostage to its demands.)

Just as U.S. natural gas via liquified natural gas, or LNG, came to the rescue during the Russian invasion of Ukraine in 2022 onward, there is a call on U.S. oil. Imagine a world that didn’t include U.S. resources now. (That thought experiment was included in a 2021 article when net zero was still a more emphatic goal as the pandemic waned.)

What is temporary or enduring depends on the Strait being reopened, which is in the interest of the entire globe now, not only the Middle East. Fortunately, the temptation to control U.S. exports is being avoided for now. In fact, it would not help U.S. prices at the pump, owing to refining issues at present. Allowing the market to flow as freely as possible now will pay dividends later. It might even calm the market to be slightly forward looking.

Illusions of a fossil-free energy world anytime to 2050 are clear. Not only is oil demand not peaking just yet, as narratives went, crude oil is expected to peak near 112 million barrels per day (m/b/d) in 2050. The year 2025 ended with supply of 106 m/b/d. It is to decline 2 m/b/d in 2026, owing to supply disruptions and demand curtailment. Several countries in Southeast Asia have begun adaptations, like rationing, supply diversifications, and other workarounds. Generally, adaptation was a climate change heuristic, and now it’s everywhere energy touches.

Price discovery of other goods is tied to the price of oil, too.

Sticker shock

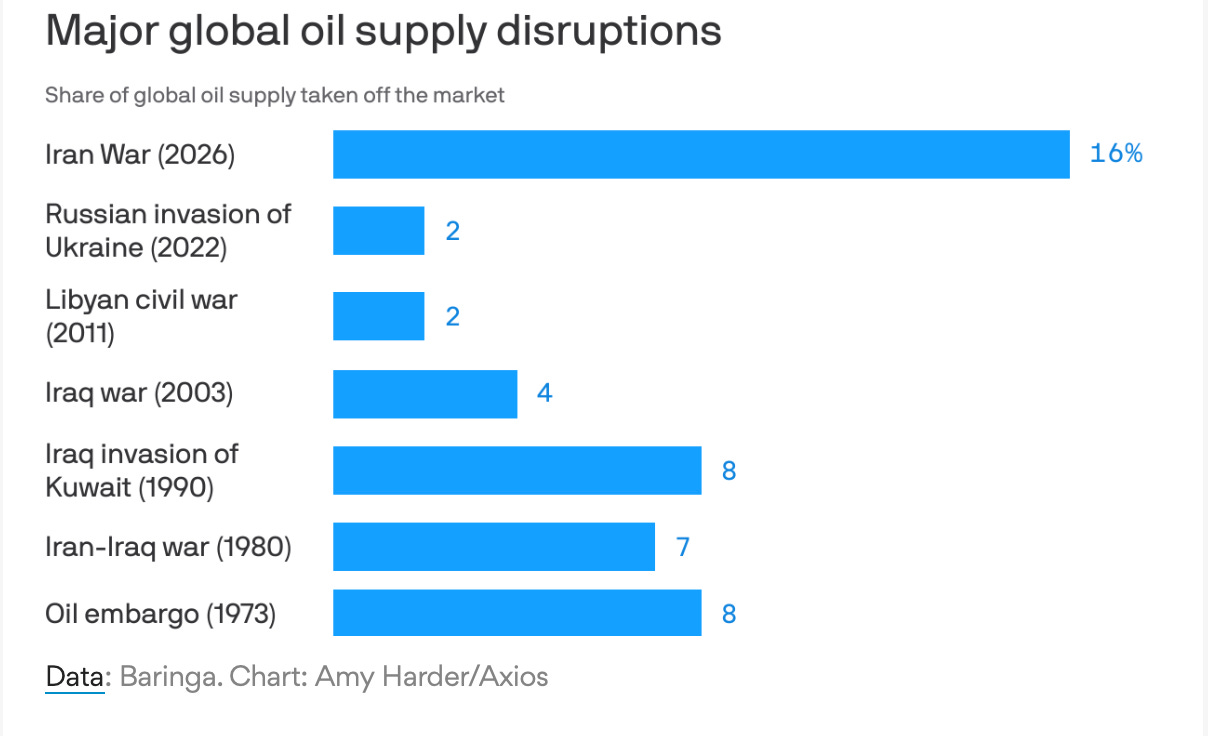

This Iran War supply shock is a big.

While this crisis is the largest disruption on record in modern history, notably the Iran War and Russian invasion included U.S. shale in the production tally, whereas earlier supply shocks did not.

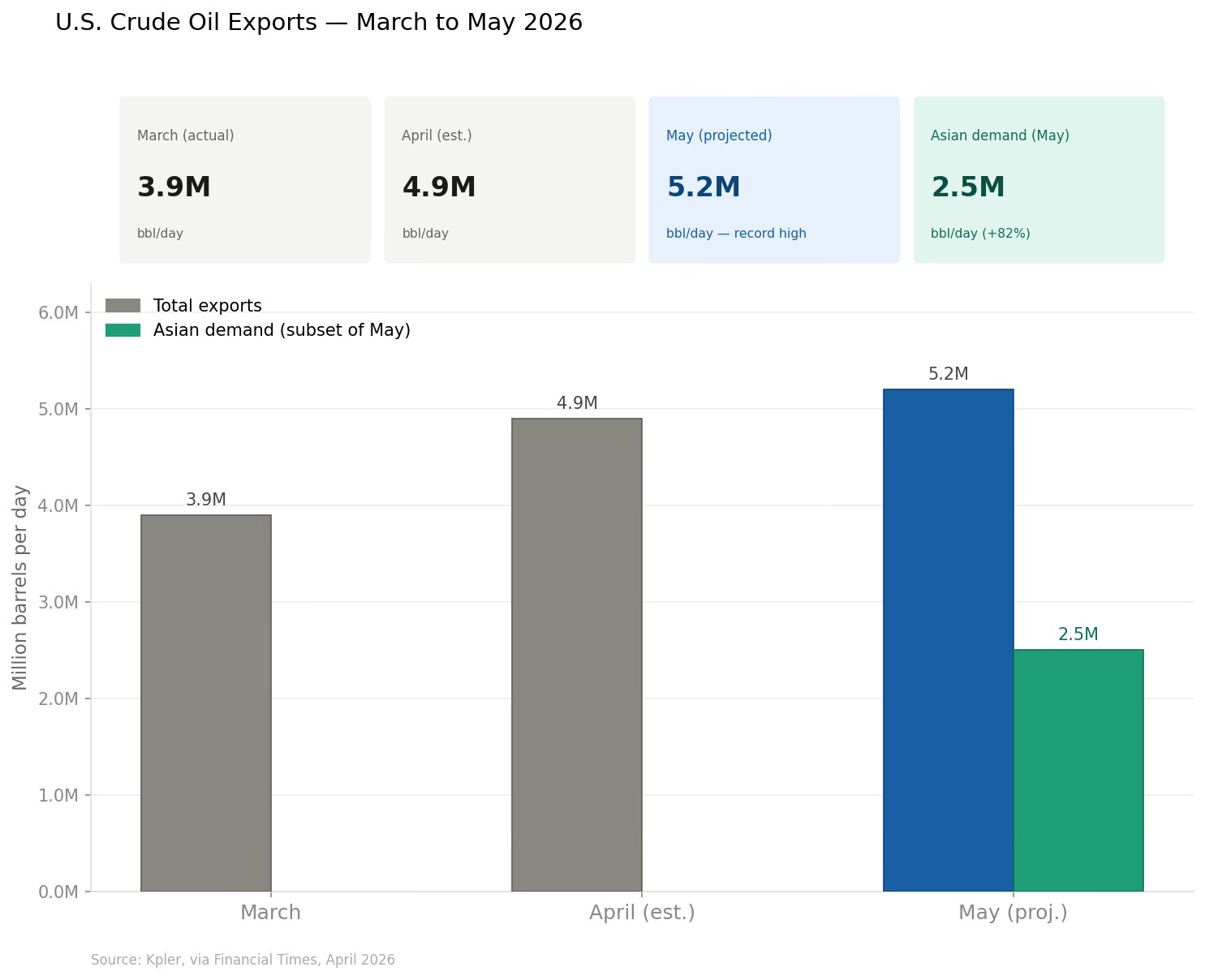

Currently, large volumes of oil are shut-in in the Middle East. OPEC recently highlighted that production has declined by 7.56 million barrels per day to 22 million in March as the closure of the Strait of Hormuz continues to create significant supply constraints. U.S. Energy Secretary Chris Wright has noted as reference that the U.S. consumes ~20 m/b/d, and the war has shut 10-15 m/b/d of supply from the Persian Gulf.

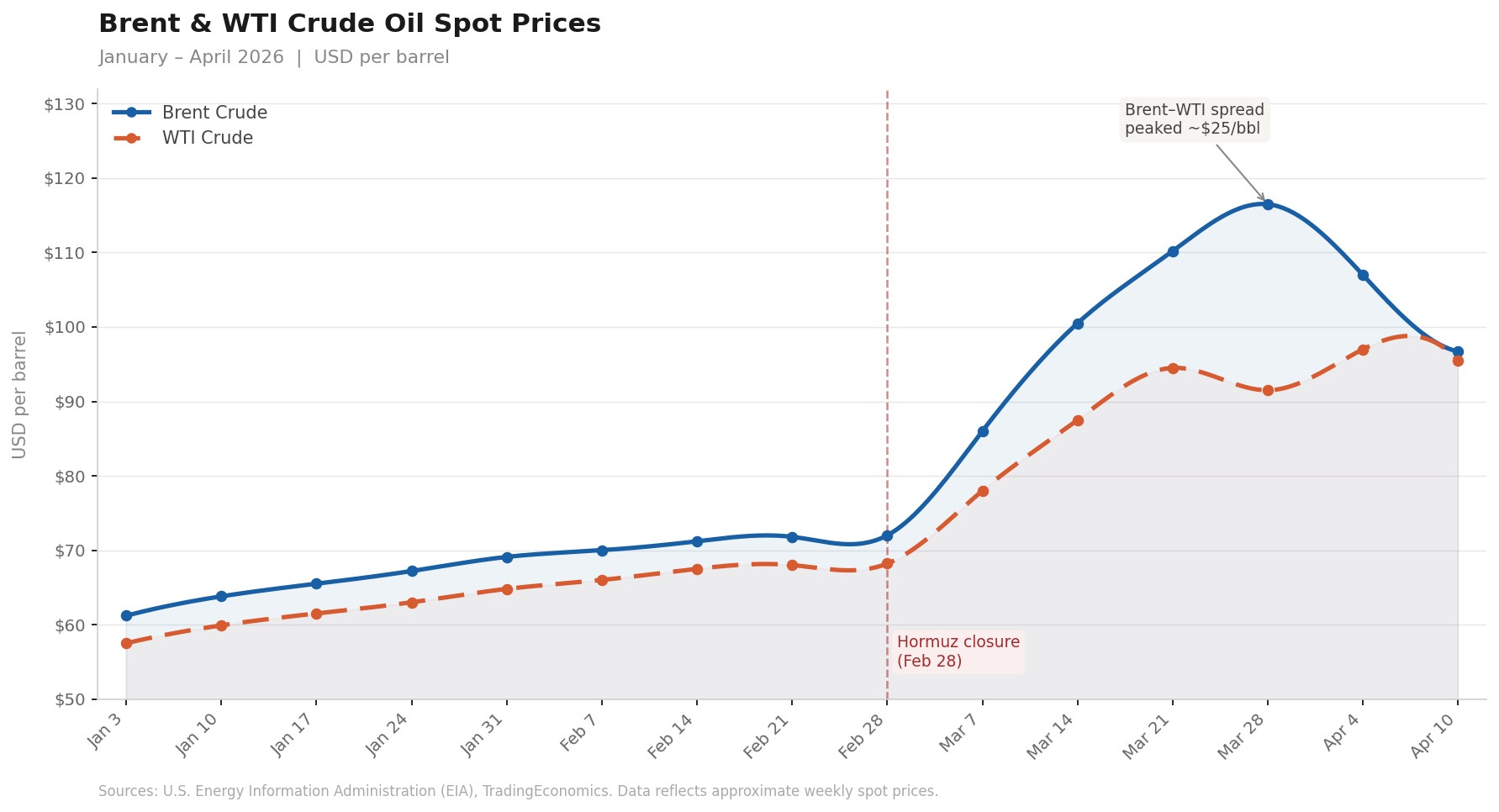

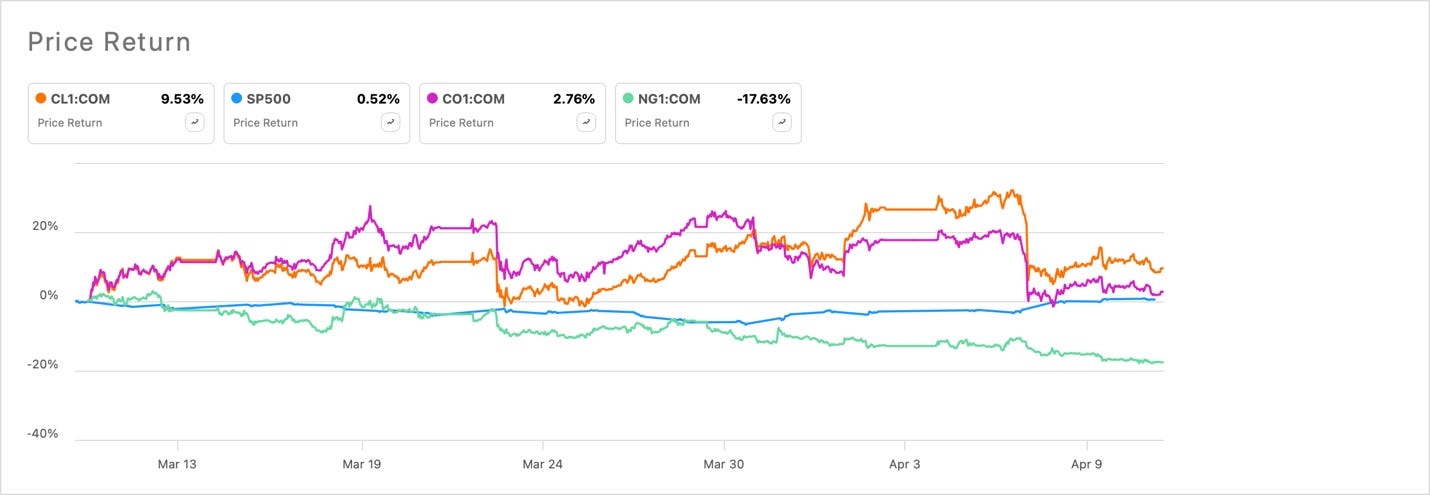

Another chart gives the actual spot prices of the conventional benchmarks. Importantly, the Dubai basket was much higher than Brent, at over $160 per barrel the week ended March 20th. The Dubai oil basket prices—which act as the primary benchmark for Middle Eastern crude oil sold to Asia—are paid primarily by Asian refiners and national oil companies. Futures prices show expectations and are generally disconnected from actual prices. Spot prices reveal the physical scarcity, as noted by a recognized analyst from Saudi Arabia at a Maguire Energy Institute symposium just days ago.

Below is the impact of WTI futures (CL1:COM) and Brent (CO1:COM). However spot prices of the physical commodity are different.

Shut in

The U.S. Energy Information Administration (EIA) says Iraq, Saudi Arabia, Kuwait, UAE, Qatar, and Bahrain collectively shut in 7.5 million barrels per day (b/d) of crude oil production in March. They expect production shut-ins will rise to 9.1 million b/d in April, assuming the conflict does not persist past April and that traffic through the Strait of Hormuz gradually resumes. Under those assumptions, they expect production shut-ins will fall to 6.7 million b/d in May and return close to pre-conflict levels in late 2026. In this best-case scenario, production resumes at full supply in late 2026, with global oil prices forecast at $96.

Just over a year ago, the relatively rapid decline in oil prices was leading a different outlook for U.S. oil and gas since the shale boom. Globally, to 2024, we had been producing 22% of the crude and liquids market and 26% of natural gas, a huge supply-side accomplishment.

I wrote last year that the pricing impact of shale has been enormous. The Dallas Fed found that oil prices in 2018 would have been roughly 36% higher had the shale revolution not occurred. Further, the shale revolution implies a reduction in current oil price volatility around 25% and a decline in long-run volatility of over 50%. Considering that the price of oil dictates so much around the world, and geopolitics were a key source of volatility, the world looks different that pre-shale. It gets taken for granted.

At the symposium last week, the analyst from Saudi Arabia said that OPEC’s control over spare capacity had also reduced volatility. However, this year spare capacity has been at record lows at 1-1.5 m/b/d, partly owing to lower prices. Currently, little oil is moving out of the Strait of Hormuz.

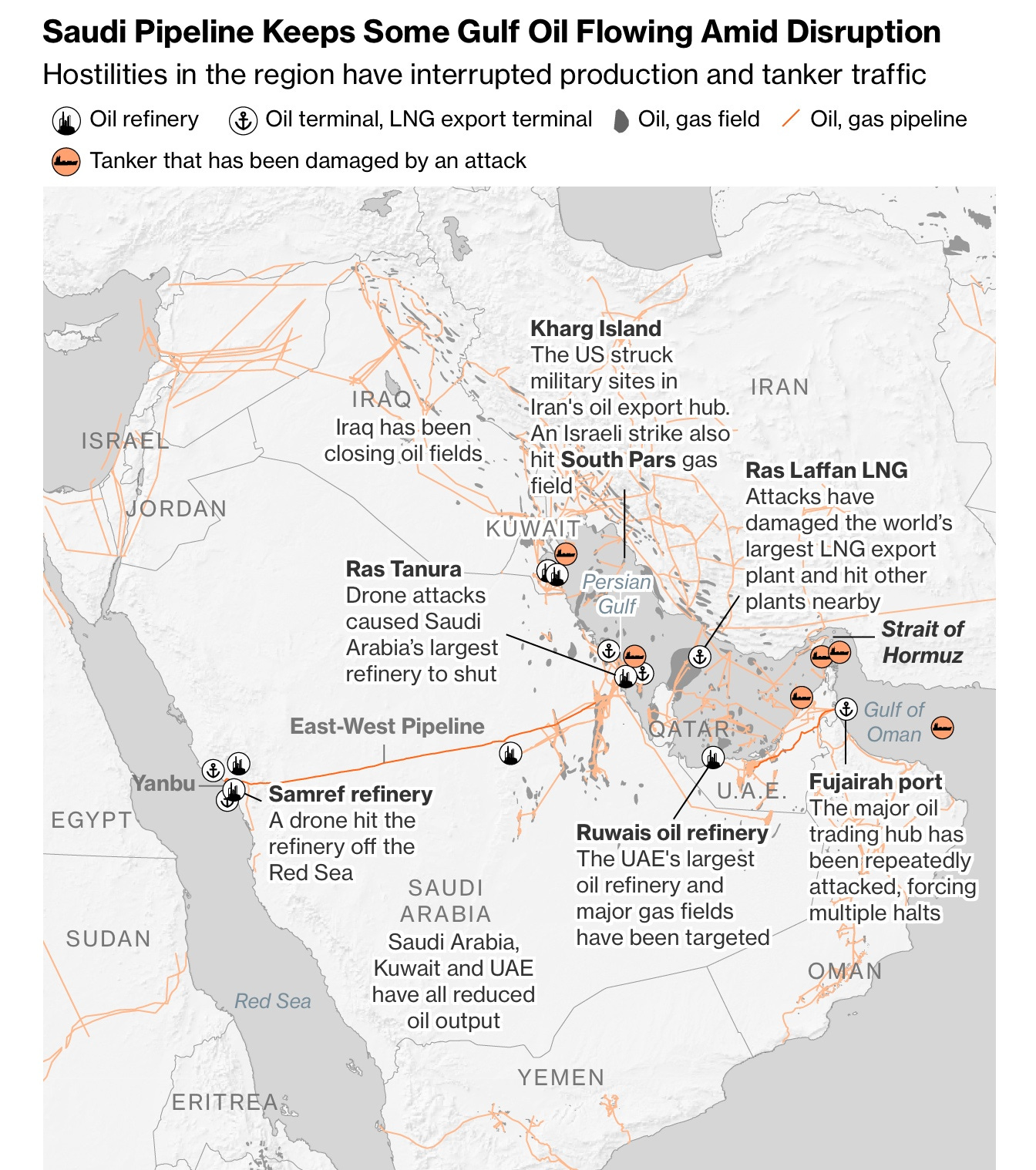

Below is a map from the EIA:

Basically, 20% of global supply moves through the Strait of Hormuz. The pipelines in the Middle East are being rethought for backup infrastructure routes, but Iran attacked the Saudi’s E-W pipeline a couple of days back. This map is from April 8th (Bloomberg).

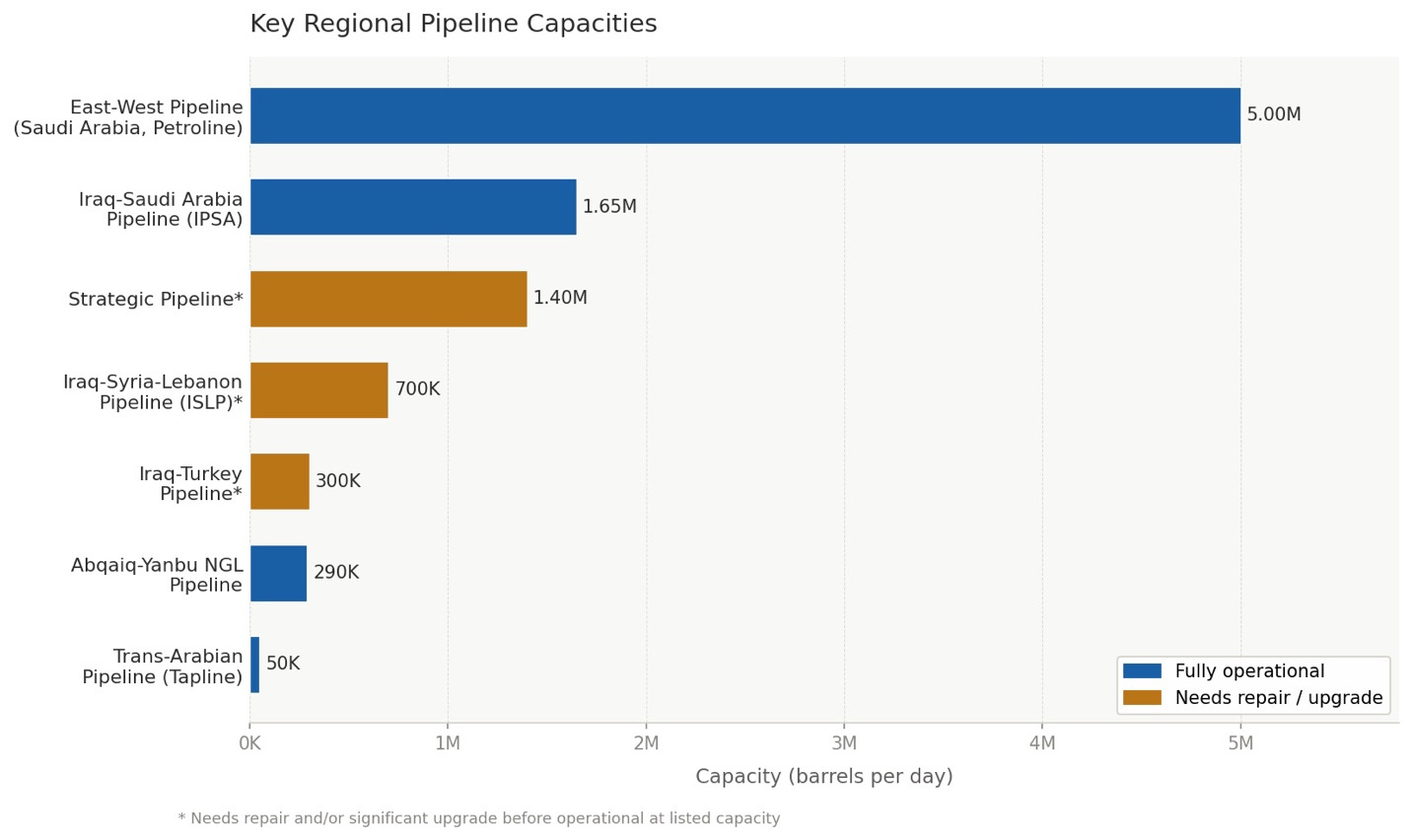

The analyst presented the following chart of some key pipelines that will be considered more valuable in the future:

Below, more color is offered for illustration purposes only about the capacity potential of various pipelines that bypass the Strait of Hormuz from the Strauss Center. (Disregard the operational status, as that has changed.) Only two are operational at present: Saudi’s E-W, with 700,000 capacity and Abqaiq-Yanbu NGL pipeline. This shows one how quickly things can change.

While the industry has faced such macroeconomic and geopolitical headwinds with aplomb in the past, the geological and economic issues surrounding peak oil are different. I’ll attempt a brief analysis that shows why it’s important. Price discovery of other goods is tied to the price of oil, too.

Opportunity: Shale and peaking supplies

Discussions of U.S. peaking oil supplies are a misnomer. Price and technological advances matter greatly in the next 10 years, especially until more nuclear capacity comes online to defray power consumption and support electrification. If anything, the density of oil, which the world relies on, has come into sharper focus. The same is true with energy sources for electrification.