Loosening The Strait's Jacket: Oil Market Creative Destruction

Gray rhino event is remaking the map, again.

The pandemic was a classic black swan event—unpredictable and unprecedented (though some would argue that). The Iran War is more of a gray rhino event, defined as a highly probable, high-impact crisis that is blatantly obvious yet widely ignored until it happens.

Like the oil futures and physical markets, the stock market and the real economy seem disconnected. U.S. consumers feel the pain at the pump and are beginning to respond accordingly. In the last week, I’ve heard from various analysts, experts, and producers in energy. Looking for new insight about the gravity and impact of the oil and gas crisis stemming from the Middle East, the most common and accurate refrain is: Nobody knows.

Those in the industry offer mixed reviews of the situation owing to the many different value chains in energy and demand centers. So what do we know about this crisis now?

The Strait of Hormuz is effectively closed. That means around 10-12% of the oil supply has been affected. More physical shortages are coming. A last count of the afflicted was 12-13 m/b/d.

(Earlier reporting)

The Flows

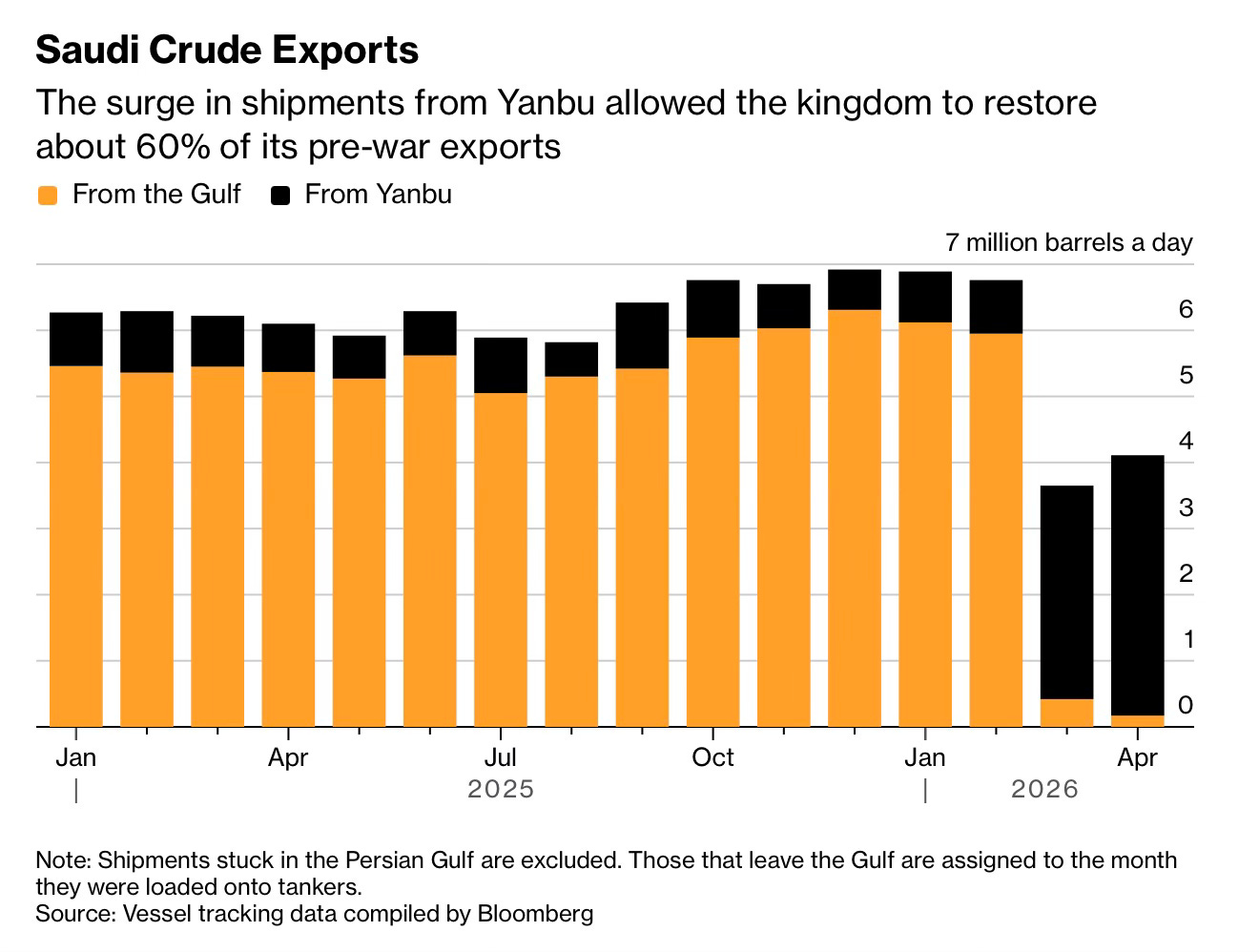

Saudi Arabia’s flows are being diverted through its East-West pipeline, the new quest to find alternatives to get product to market. Up to 5 m/b/d can be flowed this way and exported outside of Hormuz, which is happening; the pipeline could potentially hold 7 m/b/d of capacity. In fact, Aramco has received higher price realizations and itself benefited from reflowing crude away from Hormuz. Rail lines are being used to move some coveted consumer goods to the UAE.

Aramco’s Chief Executive Officer Amin Nasser said recently:

“If trade flows resume immediately or today through the Strait of Hormuz, it will take a few months for the oil market to rebalance. (However), if trade and shipping remain curtailed by more than a few weeks from today, we anticipate the supply disruption to persist, and the market to normalize only in 2027.”

Saudi Arabia’s crude oil exports are important in global markets. They now have 60% of pre-war exports online. If the UAE can ramp up as intended, more renewed barrels, which are offline from the Gulf, can offer the market an assist. The UAE could ramp up from their 3.2-3.5 m/b/d prior OPEC quota to 5 million by 2027, and conceivably higher. The “higher” option would be an unusual event but not entirely inconceivable anymore.

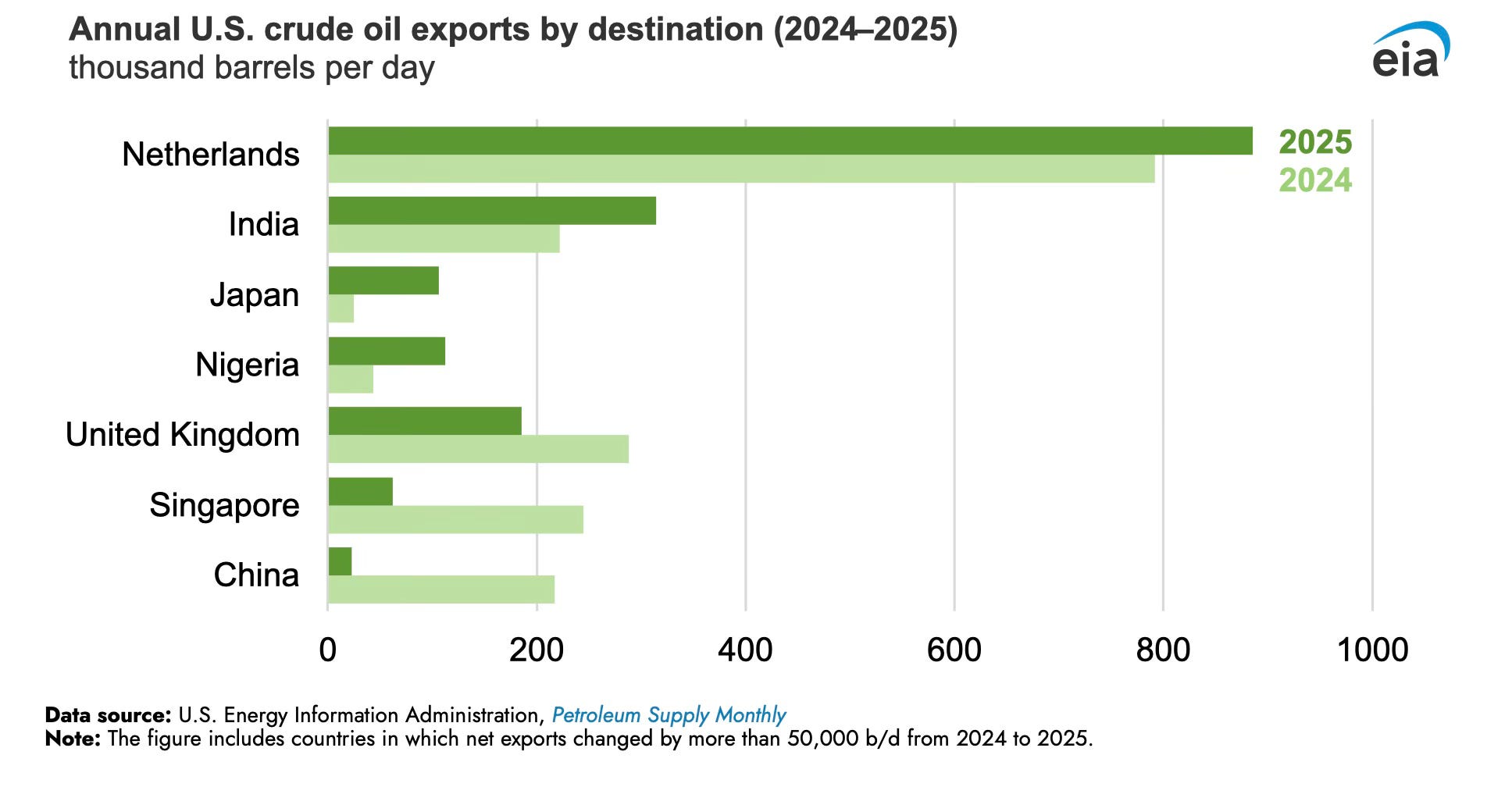

On the products side, the U.S. exported over 6 m/b/d of crude in early May from close to 4 m/b/d in April; those numbers are inching down owing to less arbitrage. That looks different for refined products: gasoline, jet fuel, and propane were up. The rest of the developing world relies heavily on hydrocarbons as a transportation fuel. These are the U.S.’s main trading partners below.

Middle East infrastructure that has been damaged and shut-in production is an upcoming problem, even when key producers attempt to restart fields. Countries more at risk include Iraq and Kuwait, and likely others, with less engineering prowess than exists in Saudi Arabia. This was an unknown impact that will come to light in the next weeks and months ahead.

The Prices

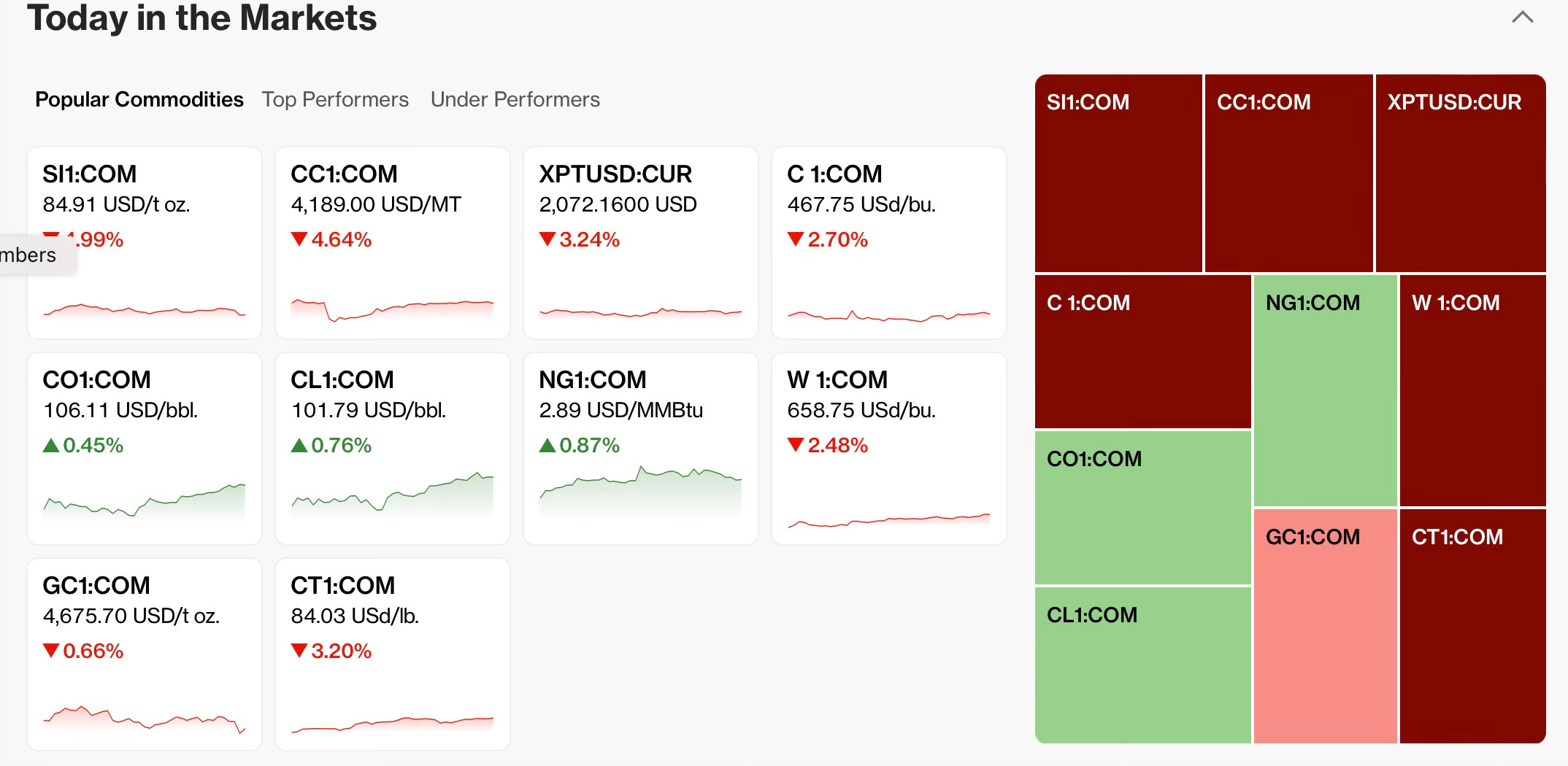

On Thursday, May 14th, both global Brent and U.S. WTI futures rose to $105 and $101, respectively. Today, WTI hit $107. The Mars oil basket, which represents the physical spot price of the medium sour crude blend that comes to U.S. Gulf ports, is $121. The differential represents the disconnect between futures prices and spot prices of the physically traded commodity. At a Dallas Federal Reserve bank event last Friday, an energy analyst discussed this Mars proxy with me.

What producers from which country will decide to produce more oil and gas to rebalance or develop new markets? This is complicated, comprised of a mix of state-owned, private, and publicly-traded firms. Many U.S. shale producers have taken a wait-and-see position, except for Diamondback and Continental Resources, which is private. Which importer countries will shift temporarily to new suppliers, or permanently? The U.S. oil patch is activated, in terms of deals and consolidation.

Another oil and gas executive noted in a presentation that physical oil traders believed $120 oil would be the price at year-end. Given the virtual stalemate in the crisis and the nonstarter Strait, this is increasingly looking plausible. As the Aramco chief executive mentioned, every week delays rebalancing. More delays to restarting oil fields add supply risk for certain Middle East producers with less capacity to pivot quicker.

The U.S. has been somewhat insulated from the impact compared to others. Where this shows up is in inflation, which has arrived and was already being experienced. Pain at the pump is the most visible effect, but it is trickling down to real budgeting and the real economy. The big question is: how will the rest of the world adjust to the crisis? The EU is planning new policies to try to shift their economic malaise to growth and rebalance their economies and trading partners.

The impacts of energy diversification and how U.S. firms reposition as a result are yet to be decided. They will flow to the U.S. in various ways from both outbound and inbound investment. Just like the outcomes are unknown of the Iran and Middle East writ-large crisis, the U.S. economy will feel some type of secondary and tertiary knock-on effects. We just don’t know exactly what. Destruction is sowing the seeds of creative destruction, with changing geopolitics, trading partners, and opportunity.