Bracing for Impact: Middle East Crisis and AI Infrastructure Build-Out

Plus Some Takeaways from the Texas Grid (with Video)

The times are strange and strained. Economic pain is being felt unequally around the globe. Supply disruptions from the Middle East conflict continue, with the situation ebbing and flowing between ceasefire and renewed hostilities.

Two notable developments: Kuwait recently called force majeure on meeting customer demands — reported on the 20th — signaling real pain felt by Gulf states and their customers. Additionally, the UAE has requested financial backstopping from the United States. This is significant given that the UAE holds sovereign wealth fund investments in U.S. AI infrastructure, including their own domestic AI build-out. Saudi Arabia has also been investing heavily in its digital infrastructure, and both countries’ plans will be impacted to varying degrees depending on how much supply remains shut in or stalled in transit.

Energy security is now top of mind globally. Countries that import from Gulf states must reckon with both short-term crisis management and medium-term diversification of energy sources. Oil prices are expected to hover in the $100-per-barrel range, and low gasoline prices in the United States are not on the horizon anytime soon.

Longer form video discussion:

Also noteworthy: reporting in the Wall Street Journal indicates an increase in militia attacks on Gulf states’ interests in Iraq — proxies acting on behalf of Iran. These attacks are becoming more diffuse, extending beyond the action connected to the Strait of Hormuz. The economic impact on Middle East and Gulf State energy-producing countries and their energy customers should not be underestimated.

U.S. AI Infrastructure Build-Out

The AI infrastructure build-out in the United States is continuing. Progress is visible on large-scale projects, including Microsoft’s $7-billion Fairwater project. Amazon recently announced a $25 billion investment in Anthropic. Microsoft has also taken over leases at the Abilene Stargate project, absorbing capacity previously held by OpenAI, Oracle CoreWeave, and Meta has absorbed some of the lease capacity too. These are enormous capital projects, and the hyperscalers have benefited from recent shifts in the competitive landscape.

The build-out is still very much active, though the intensity of near-future investment remains uncertain. Power availability remains the central constraint — the key governor on the pace of growth. A secondary constraint could emerge from inflation: higher interest rates, consumer pressure, and shifting priorities between spending on energy versus data could introduce speed bumps.

Texas Grid & Data Center Demand

Some takeaways follow that are partly from a Global Energy Symposium hosted by TCU’s energy institute, which I attended last week. Highlights include remarks from the CEO of ERCOT, the Texas grid operator, as well as an executive from power producer Vistra.

Demand Growth

The ERCOT CEO Pablo Vega confirmed that the headlines about growth are accurate. Demand is coming from data centers, industrial users, crypto mining, and oil and gas operations. Vistra estimates the Texas grid will grow at 4–6% per annum in the years ahead; PJM (the northeastern U.S. grid) is projected to grow 2–3%. Texas is attracting the lion’s share of data center development for reasons documented in a number of features and posts here.

Grid Statistics & Interconnection Queue

Texas peak demand on the grid has been approximately 85 gigawatts. The total generation queue over the coming years stands in Texas alone stands at 450 gigawatts: 360 GW from solar and batteries, 60 GW from gas, and 50 GW from wind. Not all of this will materialize.

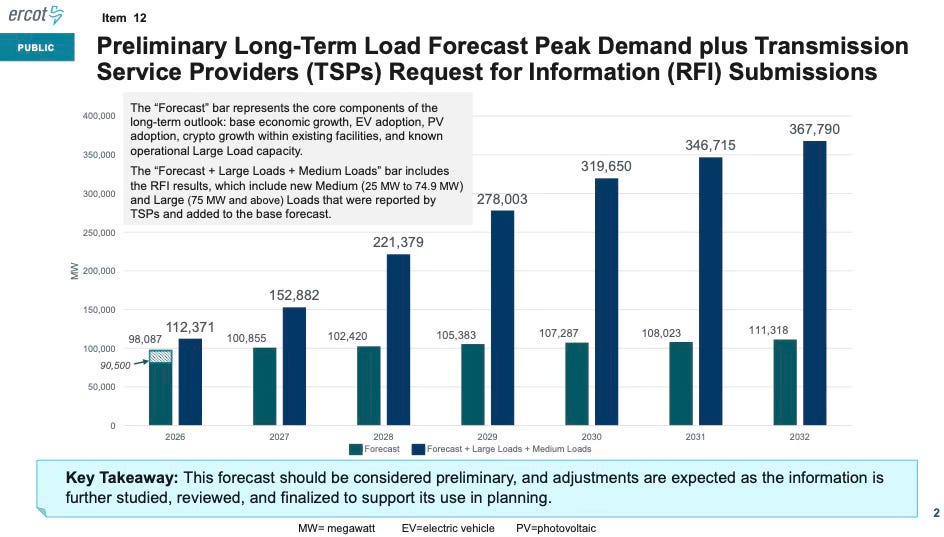

From a report of April 21, regarding preliminary large load peak demand forecasts and reported requests of interest to connect, ERCOT highlighted transmission service providers reporting about what’s in the interconnection queue. The 2026 peak demand forecast is 98 gigawatts, with 112 gigawatts reported, which speaks to near-term interest. Data center demand alone in the queue as reported by the Transmission Service Providers:

2026: 7.4 GW

2027: 40 GW

2028: ~100 GW

2029: 150 GW

2030: 187 GW

2031: 212 GW

2032: 228 GW

For context, crypto mining represents 9 GW through 2032, industrial load adds 3 GW, and oil and gas 2.5 GW. Data centers dominate. Industry analysts suggest only a fraction of the queued data center demand will actually connect — at maximum half, or likely much less.

Grid Modernization

ERCOT is moving toward a “batch process” for interconnection studies, designed to reduce uncertainty and produce more reliable forecasts. Interconnection will be aligned with transmission planning, and stricter entry criteria will govern who gets into the queue going forward.

Texas is also building new 765 kV high-voltage transmission lines — a less-common infrastructure type in the U.S. These lines are five times more efficient over long distances than the 345 kV lines which were planned two years back, and are now superseded. Initial routes will originate in far West Texas, passing through the Permian Basin, with additional lines serving the Texas Triangle (Dallas/Fort Worth-Austin/San Antonio–Houston corridor). In Texas, construction takes 5–6 years; in other states, 9–13 years, according to a panelist at the conference.

These transmission upgrades will benefit oil and gas, data centers, and industrial users to keep up with Texas’ economic growth.

(For background on the 765 kV plan and the earlier CREZ lines (built to move renewables, see the NAPE magazine article referenced in this video.)

Summary

The Middle East crisis continues and impacts are being felt. Its economic impact — on Gulf states, their customers, and the global energy market — deserves diligent attention, not to be underestimated. In the United States, the effects so far have been rising inflation and higher prices at the pump. If the crisis persists, capital projects will increasingly compete, interest rates will constrain investment, and the AI infrastructure build-out may face some headwinds.

Two governors are at work on the pace of AI infrastructure growth: power availability, and the broader macroeconomic environment shaped by energy costs, inflation, and interest rates. The digital economy is not going away — but there may be speed bumps ahead.

This crisis reminds us how interconnected the global economy still is, especially through energy.

Other reference chart from ERCOT: